₹1 crore.

In India, that number carries enormous weight. It is the dream salary. The aspirational savings target. The price tag on a decent flat in a decent city. The number that makes your parents proud and your relatives quiet at family gatherings.

But what does ₹1 crore actually buy you — in real life, in real purchasing power, in real quality of living — when you compare India with Dubai?

The answer is not what most people expect. And once you see the real numbers side by side, the way you think about money, lifestyle, and where you choose to live will never be quite the same.

We are going to look at ₹1 crore across six different dimensions — as a salary, as savings, as real estate, as a monthly lifestyle, as an investment, and as a retirement fund. Every number in this article is real, current, and verifiable.

Before reading further — use our free Salary Calculator to see exactly how much your current salary would be worth in Dubai after conversion. The result might surprise you too.

Context First — How ₹1 Crore Converts to Dubai Money

At the current exchange rate of AED 1 = ₹23 (May 2026), ₹1 crore equals approximately AED 4,35,000 — or roughly $118,000 USD.

But raw currency conversion is misleading. The real question is not what ₹1 crore converts to in dirhams — it is what ₹1 crore achieves in each location. Purchasing power, tax treatment, investment returns, and lifestyle cost all determine the true value of money. And on every one of those dimensions, the comparison between Dubai and India produces genuinely shocking results.

1. ₹1 Crore as an Annual Salary

In India

₹1 crore per year — approximately ₹8.33 lakh per month — puts you in the top 1% of Indian earners. It sounds extraordinary. And in Indian terms, it genuinely is.

But here is what actually happens to ₹1 crore annual salary in India after tax and living costs:

| Item | Amount | Notes |

|---|---|---|

| Gross Annual Salary | ₹1,00,00,000 | ₹1 crore |

| Income Tax (30% slab + surcharge + cess) | -₹31,20,000 | Effective rate ~31.2% |

| EPF Contribution | -₹1,80,000 | Mandatory 12% of basic |

| Take-Home Salary | ₹67,00,000 | ₹5.58 lakh/month |

| Annual Living Cost (Mumbai — family of 3) | -₹36,00,000 | ₹3 lakh/month all-in |

| EMI on home loan (₹2 crore flat at 8.5%) | -₹18,00,000 | ₹1.5 lakh/month for 20 yrs |

| Annual Savings | ₹13,00,000 | ₹1.08 lakh/month |

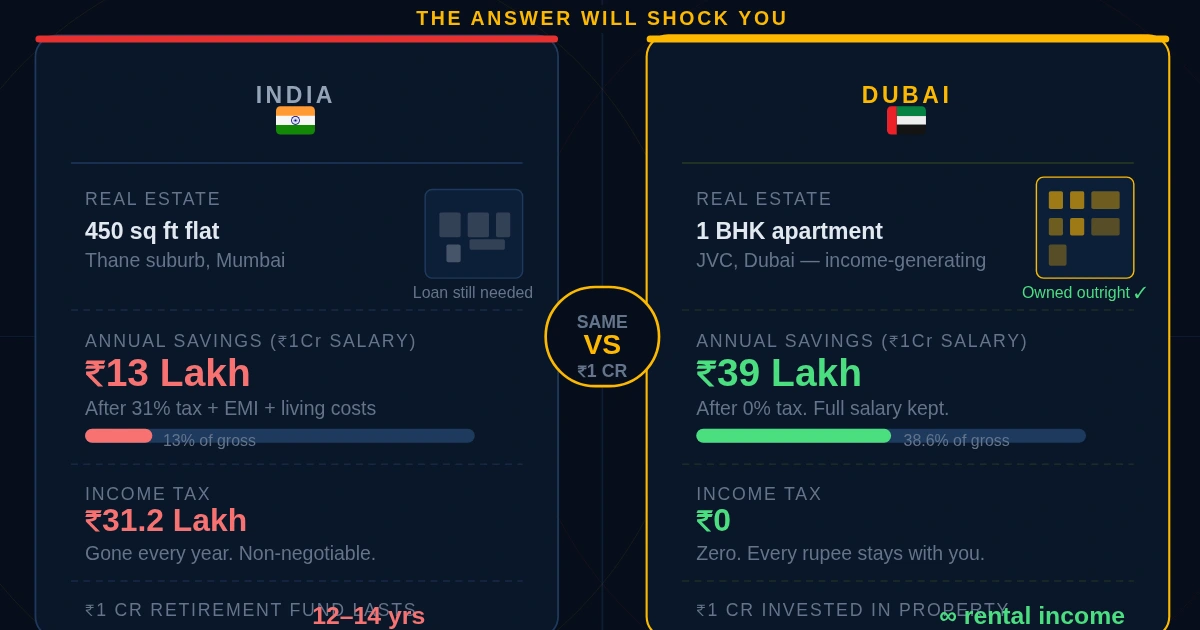

So ₹1 crore annual salary in India — after tax, after living costs, after EMI on a decent home — leaves you saving approximately ₹13 lakh per year. That is 13% of your gross income. And this assumes Mumbai-level costs — Bangalore and Delhi are comparable.

In Dubai

Now look at what ₹1 crore annual salary looks like for the equivalent professional in Dubai — earning AED 4,35,000/year (AED 36,250/month):

| Item | Amount (AED) | Amount (₹) |

|---|---|---|

| Gross Annual Salary | AED 4,35,000 | ₹1,00,05,000 |

| Income Tax | AED 0 | ₹0 |

| Social Security | AED 0 | ₹0 (for expats) |

| Take-Home Salary | AED 4,35,000 | ₹1,00,05,000 |

| Annual Living Cost (family of 3, mid-range) | AED 1,80,000 | ₹41,40,000 |

| Rent (2BHK Dubai — mid area) | AED 85,000 | ₹19,55,000 |

| Annual Savings | AED 1,70,000 | ₹39,10,000 |

The verdict: The same ₹1 crore salary in Dubai generates ₹39 lakh in annual savings compared to ₹13 lakh in India. That is 3 times more savings from the exact same nominal income — purely because of 0% tax and lower cost relative to salary.

Put another way: in Dubai, you save in 4 months what takes a full year to save in India on the same salary.

2. ₹1 Crore in Real Estate — What Property Does It Buy?

This is where the comparison becomes genuinely jaw-dropping.

In India

₹1 crore in Indian real estate buys you:

| City | What ₹1 Crore Buys | Area | Neighbourhood |

|---|---|---|---|

| Mumbai | 1 BHK flat | 450–550 sq ft | Thane, Navi Mumbai (periphery) |

| Bangalore | 2 BHK flat | 900–1,100 sq ft | Whitefield outskirts, Electronic City |

| Delhi NCR | 2 BHK flat | 800–1,000 sq ft | Noida, Ghaziabad, Faridabad |

| Hyderabad | 2–3 BHK flat | 1,000–1,200 sq ft | Kondapur, Miyapur, Bachupally |

| Chennai | 2 BHK flat | 900–1,000 sq ft | Tambaram, Pallavaram (suburbs) |

In Mumbai — India's financial capital and the aspirational address for millions — ₹1 crore buys you a 450 sq ft apartment in a suburb, with a 20-year home loan still required for most buyers even at this price point.

In Dubai

₹1 crore = AED 4,35,000. In Dubai real estate, this buys you:

| Property Type | Area | Location | Annual Rental Income |

|---|---|---|---|

| Studio apartment | 400–500 sq ft | Dubai Marina, JLT | AED 45,000–55,000/yr |

| 1 BHK apartment | 650–800 sq ft | Sports City, JVC, Al Furjan | AED 55,000–70,000/yr |

| 1 BHK apartment | 700–900 sq ft | Dubai South, Dubailand | AED 50,000–65,000/yr |

| Plot of land | 2,000–3,000 sq ft | Outer Dubai areas | N/A (build your own) |

At AED 4,35,000, you can buy a fully furnished 1 BHK apartment in Dubai that:

- Generates rental income of AED 55,000–70,000/year (~₹12.65–₹16.1 lakh/year)

- Appreciated 16–22% in value in 2023–2024 alone

- Is freehold — you own it outright, no loan needed at this price point

- Has no property tax, no capital gains tax on sale

- Can be listed on Airbnb as a short-term rental — generating AED 80,000–1,20,000/year

The verdict: ₹1 crore in Mumbai buys you a tiny suburb apartment that you still need a loan to maintain. ₹1 crore in Dubai buys you a fully owned income-generating property in a globally recognised city — with zero tax on the rental income and zero tax when you sell it.

Curious what your Dubai property investment could earn? See real listings on our UAE Opportunities page.

3. ₹1 Crore as Monthly Lifestyle — What Does It Actually Fund?

Let us flip the perspective. Instead of annual salary, let us ask: what monthly lifestyle does ₹1 crore of annual income fund in each city?

₹1 crore annually = ₹8.33 lakh/month gross in India. After tax: ₹5.58 lakh/month.

₹1 crore annually = AED 36,250/month in Dubai. After tax: AED 36,250/month (0% tax).

| Lifestyle Element | India (Mumbai) | Dubai | Winner |

|---|---|---|---|

| Home | 2 BHK rent — ₹70,000/mo in Bandra | 2 BHK rent — AED 7,500/mo in JVC (~₹1.72L/mo) | 🇮🇳 India (cheaper rent) |

| Domestic help | Cook + maid — ₹15,000/mo | Live-in helper — AED 1,200/mo (~₹27,600/mo) | 🇮🇳 India (far cheaper) |

| Car | Sedan EMI — ₹25,000/mo | Sedan — AED 1,500/mo lease (~₹34,500/mo) | 🇮🇳 India (marginally) |

| Children's school | Premium school — ₹2.5L/year | Good CBSE school — AED 20,000/year (~₹4.6L) | 🇮🇳 India (cheaper) |

| Dining out (4x/month) | ₹8,000/mo (family) | AED 800/mo (~₹18,400) | 🇮🇳 India (cheaper) |

| Healthcare | Private insurance ₹40,000/year | Company-provided (free) | 🇦🇪 Dubai (free) |

| Air quality | AQI 150–300 (poor to hazardous) | AQI 30–60 (good) | 🇦🇪 Dubai (far better) |

| Safety | Moderate — varies by area | One of world's safest cities | 🇦🇪 Dubai (far better) |

| Annual flights to India | N/A | AED 800–1,200 return (~₹18,400–₹27,600) | 🇮🇳 India |

| Take-home surplus/month | ₹1,08,000/mo | AED 14,000/mo (~₹3,22,000/mo) | 🇦🇪 Dubai (3x more) |

The verdict: India wins on individual cost items — rent, domestic help, food are genuinely cheaper. But Dubai wins on what actually matters — the money left over after everything is paid. A ₹1 crore earner in Dubai keeps 3 times more of their income every single month, which means wealth building happens 3 times faster.

4. ₹1 Crore as an Investment — Where Does It Grow Faster?

Let us compare what happens when you invest ₹1 crore in each country's most accessible investment vehicles.

India — Fixed Deposit (Safest Option)

- Current FD rate: 7–7.5% per annum

- Interest earned: ₹7–7.5 lakh/year

- Tax on interest (30% slab): -₹2.1–₹2.25 lakh

- Net annual return: ₹4.75–₹5.25 lakh (~5%)

- Inflation rate: 5–6% per annum

- Real return after inflation: Near zero to negative

Dubai — High-Interest Savings Account / Investment

- AED equivalent: AED 4,35,000

- UAE bank savings rate: 4–5% per annum

- Interest earned: AED 17,400–21,750/year (~₹4–5 lakh)

- Tax on interest: AED 0 (0% tax)

- Net annual return: Full AED 17,400–21,750 (~₹4–5 lakh)

Nominal returns appear similar. But the critical difference is tax treatment. In India, your FD interest is taxed at your income slab rate — meaning a ₹1 crore earner pays 30% tax on FD interest, wiping out a third of returns. In Dubai, interest income carries zero tax. The full return stays with you.

Dubai Real Estate — The Real Investment Case

Now look at what ₹1 crore invested in Dubai real estate has actually done in recent years:

| Year | Dubai Property Price Growth | Rental Yield | Total Annual Return |

|---|---|---|---|

| 2022 | +11.3% | 5.8% | 17.1% |

| 2023 | +19.6% | 6.1% | 25.7% |

| 2024 | +16.8% | 6.3% | 23.1% |

| 2025 | +12.4% | 6.5% | 18.9% |

₹1 crore invested in Dubai real estate in 2022 (AED 4,35,000) would be worth approximately AED 7,50,000–8,00,000 today — a gain of AED 3,15,000–3,65,000 (~₹72–84 lakh) in 3 years. Plus rental income of AED 1,05,000 over the same period (~₹24 lakh). Total return: ₹96–₹1.08 crore on a ₹1 crore investment in 3 years. Tax free.

Compare that to an Indian FD on the same ₹1 crore over 3 years at 7% post-tax: approximately ₹15.75 lakh in net interest after tax.

The verdict: Dubai real estate has returned more in 1 year than Indian FD returns in 6–7 years — and every rupee of that gain is tax-free.

5. ₹1 Crore as Retirement Savings — How Long Does It Last?

This is perhaps the most personal comparison of all. ₹1 crore saved for retirement — how long does it actually last in each location?

In India (Tier 1 City — Mumbai/Delhi/Bangalore)

| Monthly Expense Category | Amount |

|---|---|

| Rent (owned home — no rent) or maintenance | ₹15,000 |

| Groceries and food | ₹25,000 |

| Healthcare (senior-specific) | ₹20,000 |

| Transport and utilities | ₹12,000 |

| Entertainment and lifestyle | ₹15,000 |

| Inflation buffer | ₹13,000 |

| Total Monthly | ₹1,00,000 |

At ₹1 lakh/month in a Tier 1 city — which is a modest retirement by most standards — ₹1 crore lasts approximately 8–9 years. Add investment returns of 5% post-tax and it stretches to perhaps 12–14 years. For someone retiring at 55, that falls short of a comfortable retirement.

In a Tier 2 Indian City (Pune, Jaipur, Coimbatore)

At ₹55,000–₹65,000/month, ₹1 crore lasts 14–18 years with returns. More manageable — but still tight for a 30-year retirement horizon.

In Dubai (As a Non-Resident Owner)

Here is an alternative retirement model that thousands of Indians are now pursuing: use ₹1 crore to buy a Dubai apartment outright. Rent it out. Live in a lower-cost country (India, Portugal, or Southeast Asia) on the rental income.

- Property purchase: AED 4,35,000 (₹1 crore)

- Annual rental income: AED 55,000–70,000/year

- Tax on rental income: AED 0

- INR equivalent at current rates: ₹12.65–₹16.1 lakh/year

- Monthly income: ₹1.05–₹1.34 lakh/month — indefinitely

- Capital value of property: Growing at 10–15% annually

The verdict: ₹1 crore spent on retirement living in India lasts 12–14 years. ₹1 crore invested in Dubai real estate generates retirement income of ₹1+ lakh/month forever — while the underlying asset appreciates. This is why thousands of Indian families are now buying Dubai property as retirement planning.

6. ₹1 Crore as an Annual Lifestyle Budget — The Fun Comparison

Finally let us get specific. ₹1 crore as an annual lifestyle budget — AED 4,35,000/year or ₹83,333/month. What does that actually look like as a daily life in each city?

Life on ₹1 Crore Annual Budget in Mumbai

- 🏠 2 BHK flat in Powai or Andheri: ₹45,000/month rent

- 🚗 Honda City on loan: ₹22,000 EMI

- 🍽️ Home cooking + 6 restaurant meals/month: ₹18,000

- 👨👩👧 Children's school (decent private): ₹15,000/month

- 🏥 Health insurance family: ₹4,000/month

- 💡 Utilities, phone, internet: ₹6,000/month

- ✈️ 1 holiday per year: ₹1,50,000

- 👗 Clothing and personal: ₹8,000/month

- 💰 Monthly savings after tax: ₹1,08,333/month

- 📊 Annual savings: ₹13 lakh (13% of gross)

Life on ₹1 Crore Annual Budget in Dubai (Tax-Free)

- 🏠 2 BHK flat in JVC or Al Furjan: AED 7,000/month rent

- 🚗 Toyota Camry on lease: AED 1,800/month

- 🍽️ Home cooking + 8 restaurant meals/month: AED 2,500

- 👨👩👧 Children's CBSE school: AED 1,500/month

- 🏥 Company medical insurance: AED 0 (employer-provided)

- 💡 Utilities, phone, internet: AED 800/month

- ✈️ 2 India trips per year + 1 international: AED 8,000

- 👗 Clothing and personal: AED 1,200/month

- 💰 Monthly savings: AED 14,000/month (₹3,22,000)

- 📊 Annual savings: AED 1,68,000 (₹38.64 lakh — 38.6% of gross)

The verdict: Same ₹1 crore. Dubai lifestyle includes a bigger apartment, a better car, international holidays, and still saves ₹38.64 lakh per year — nearly 3 times more than Mumbai despite living better.

The One Number That Changes Everything

Here is the single most important number in this entire comparison:

Over 10 years — without any investment growth — that difference compounds to:

- India total savings: ₹1.3 crore

- Dubai total savings: ₹3.9 crore

- Difference: ₹2.6 crore — on the exact same salary

That ₹2.6 crore difference is not earned through a better job, a smarter investment, or a lucky break. It is the pure mathematical consequence of geography and tax policy.

So What is the Catch?

This article has made Dubai sound like an obvious choice. So why doesn't everyone go? Because the comparison is real but so are the trade-offs. Here is what Dubai cannot give you:

- Permanent roots — UAE has no standard PR for most expats. You are always an employee visa holder — your legal right to stay depends on employment

- Family proximity — flights are easy and affordable but you are not around for everyday family moments

- Domestic help is expensive — a live-in maid costs AED 1,200–1,500/month vs ₹8,000–₹12,000 in India

- Summers are brutal — May to September reaches 45–48°C. Outdoor life essentially stops

- Cultural adjustment — some Indians struggle with the transient nature of expat life where friendships change as people come and go

- No guaranteed future — if you lose your job, your visa status is immediately affected

For those who want permanent residency and long-term settlement, Canada and Australia offer clearer pathways — with their own salary and lifestyle trade-offs. Our Find My Path tool helps you weigh all these factors based on your specific situation.

The Bottom Line — What ₹1 Crore Really Buys You

| Category | India (Mumbai) | Dubai | Advantage |

|---|---|---|---|

| Annual savings (₹1Cr salary) | ₹13 lakh | ₹39 lakh | 🇦🇪 Dubai (3x) |

| Real estate bought outright | 450 sq ft suburb flat | 1 BHK income-generating apartment | 🇦🇪 Dubai |

| Investment return (post-tax) | ~5% real return | 15–23% (real estate) | 🇦🇪 Dubai |

| Retirement duration | 12–14 years | Indefinite rental income | 🇦🇪 Dubai |

| Monthly lifestyle quality | Good | Excellent | 🇦🇪 Dubai |

| Safety and air quality | Moderate | World-class | 🇦🇪 Dubai |

| Family roots and culture | Deep | Limited | 🇮🇳 India |

| PR and permanence | Home country | None (employment dependent) | 🇮🇳 India |

| Domestic help cost | Affordable | Expensive | 🇮🇳 India |

The numbers are clear. Dubai wins on every financial metric — savings rate, investment returns, purchasing power, and retirement planning. India wins on permanence, family, culture, and affordable domestic lifestyle.

The real question is never "which city has better numbers." It is always "which city fits where I am in life right now."

If you are 28–42, career-driven, and want to build wealth at 3x the speed — the numbers make Dubai almost impossible to argue against for a 5–10 year stint.

If you are 50+, rooted, and value permanence over financial optimisation — India makes complete sense.

Most people who read this article are in the first category. And they already know, deep down, what the numbers are telling them.

Ready to find out what your specific salary would be worth in Dubai? Use our free International Salary Calculator — enter your current India salary and see your Dubai take-home, monthly savings, and how many years it would take to hit ₹1 crore in savings. Also check our complete UAE Guide for visa, cost of living, and top companies hiring right now.

0 Comments

Have a question or insight? Share it below. All comments are moderated within 24 hours.

Be the first to share your thoughts.

Leave a Comment

Your email will not be published. Fields marked * are required.